![[Industry Direct] PHI Studio & Agog Are Seeking Immersive Artists for a Four Week Residency Program](https://roadtovrlive-5ea0.kxcdn.com/wp-content/uploads/2025/05/phi-immersive-residency-2-341x220.jpg?#)

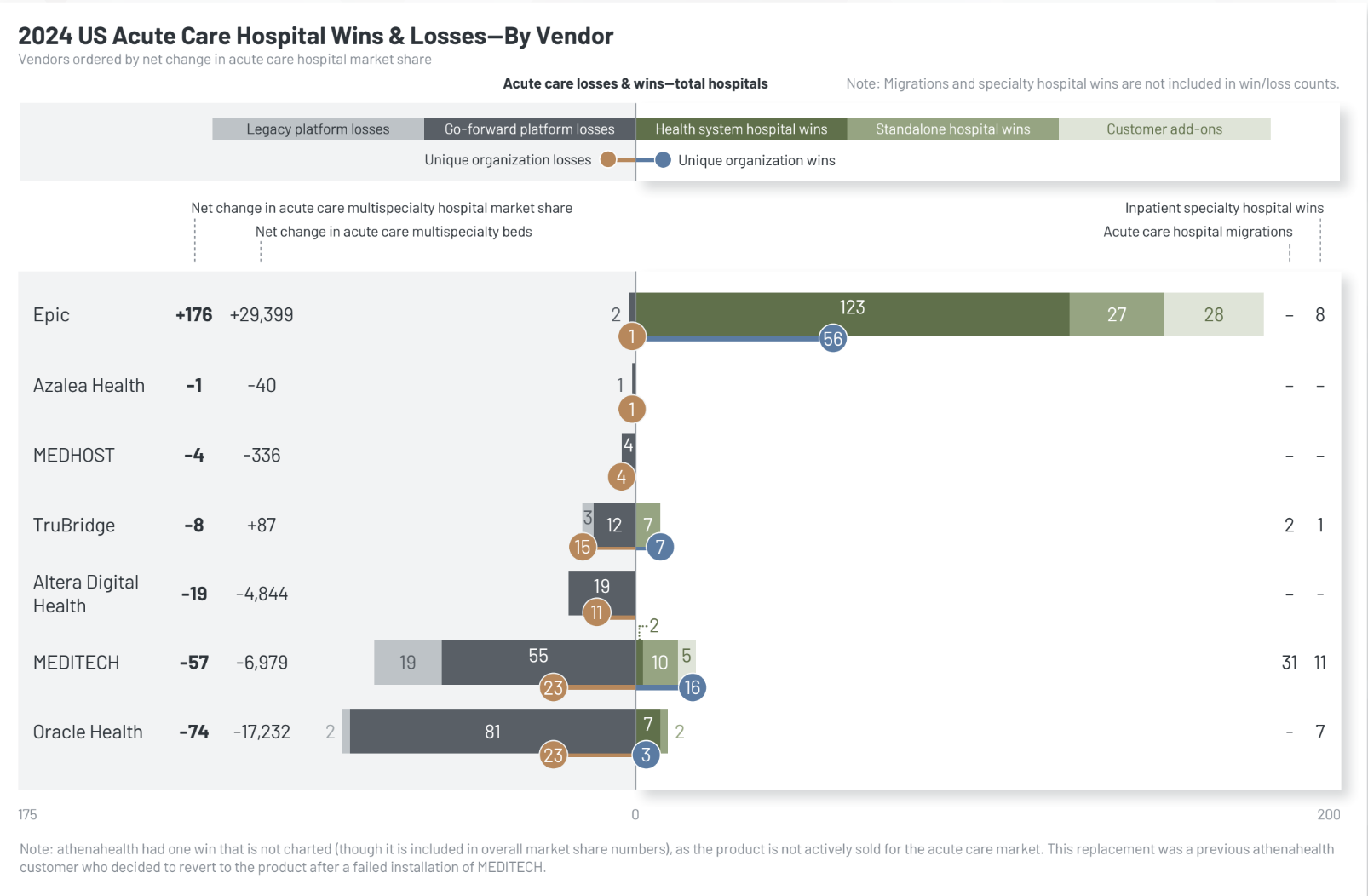

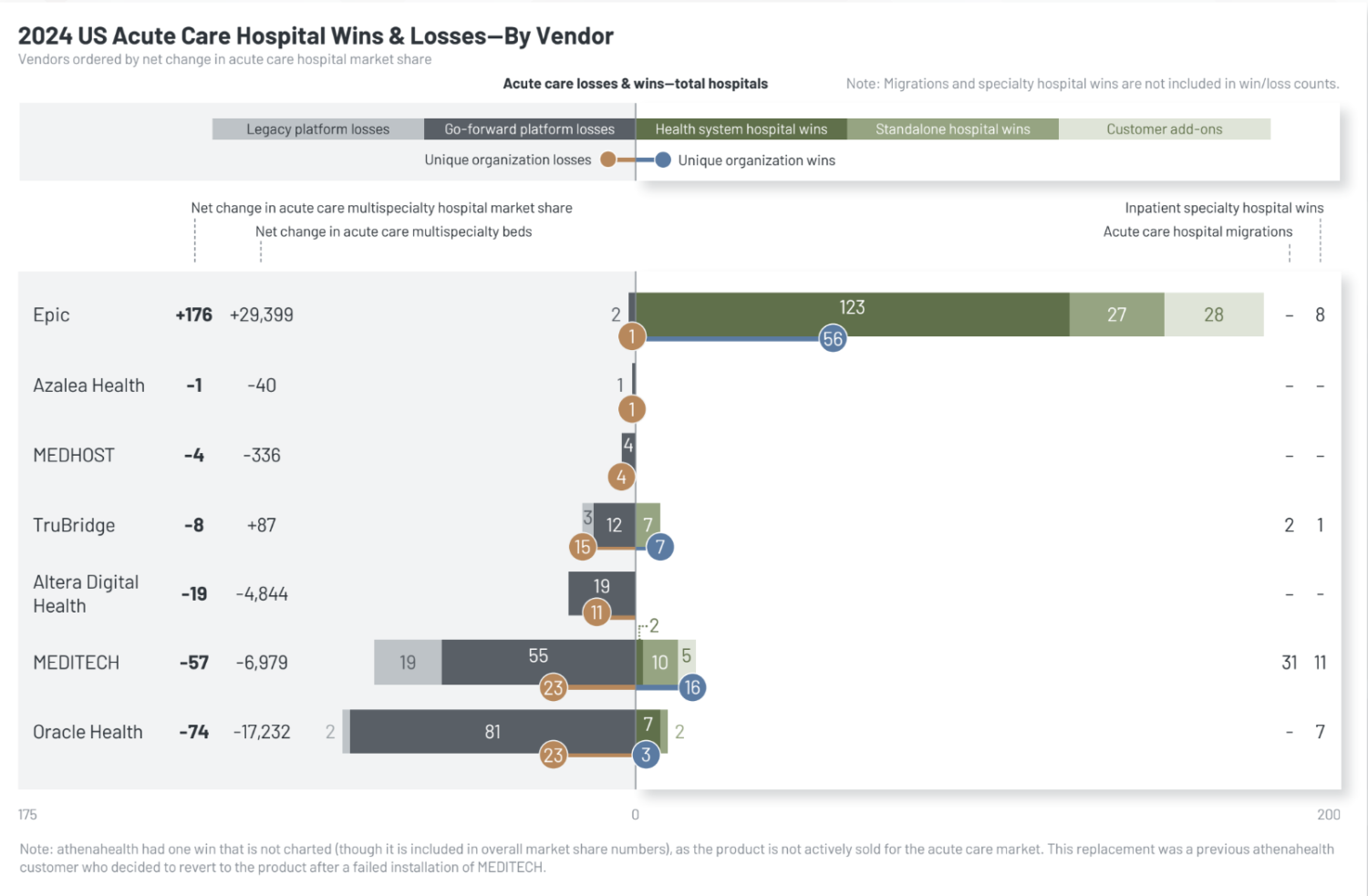

KLAS: Epic Dominates 2024 EHR Market Share Amid Focus on Vendor Partnership; Oracle Health Sees Losses Despite Tech Advances

What You Should Know: – The strength of the vendor-customer partnership emerged as a critical factor influencing Electronic Health Record (EHR) purchasing decisions in the US acute care market during 2024, according to the latest report from KLAS Research. – While overall purchasing energy cooled slightly compared to the previous year, large health systems continued ... Read More

What You Should Know:

– The strength of the vendor-customer partnership emerged as a critical factor influencing Electronic Health Record (EHR) purchasing decisions in the US acute care market during 2024, according to the latest report from KLAS Research.

– While overall purchasing energy cooled slightly compared to the previous year, large health systems continued to drive the majority of decisions, often favoring vendors perceived as strong partners who listen to feedback and deliver on promises. The “US Acute Care EHR Market Share 2025” report analyzes purchase decisions made between January and December 2024

Epic Extends Market Lead with Record Gains

Epic solidified its dominant position in the US acute care EHR market, achieving its largest net gain on record in 2024, adding 176 hospitals. This continues a decade-long trend where Epic has been the exclusive choice for large health systems making strategic, go-forward EHR decisions. In 2024, 10 large health systems selected Epic, accounting for 108 hospitals (with 67 hospitals coming from just two organizations).

Decisions favoring Epic were frequently driven by the platform’s stability, robust interoperability capabilities, generally high customer satisfaction, and a strong reputation for partnership. Epic also secured the most wins among small standalone hospitals (<200 beds) in 2024, largely attributed to the stable experience provided through its Community Connect program. Overall, Epic captured nearly 70% of all hospital EHR decisions made during the year. Despite its dominance, KLAS notes that the significant cost and resource requirements for implementation remain the primary barrier for large systems considering, but not yet switching to, Epic. As of the end of 2024, Epic holds an estimated 42.3% of the US acute care hospital market share and 54.9% of the bed market share.

Oracle Health Faces Challenges Despite Tech Optimism

Oracle Health experienced a challenging year, seeing a net loss of 74 hospitals in 2024. KLAS noted that Oracle Health declined to share its list of new contracts for the first time, requiring KLAS to rely on public sources and internal research, making the win/loss counts estimates, particularly for smaller hospitals. Only 9 new hospital wins were identified by KLAS (2 standalone, 1 system of 7).

Long-standing customer concerns regarding poor partnership and a lack of follow-through on promises persist. Customer ratings for loyalty and relationship have dropped significantly (over 10 points) since the period just before Oracle’s acquisition of Cerner was announced in late 2021. However, there are signs of cautious optimism among some customers. Recent major technology developments announced or implemented in 2023 and 2024, such as the Clinical AI Agent, Seamless Exchange, Oracle Cloud Infrastructure integration, and plans for a new EHR and patient portal, have garnered interest. Reflecting this, KLAS pulse checks indicate over a third of surveyed customers saw a positive change in Oracle Health’s execution and delivery over the last six months of 2024, a notable shift from recent sentiment. Oracle Health holds an estimated 22.9% of the hospital market share and 22.1% of the bed market share.

MEDITECH Shows Strong Legacy Retention but Loses Ground Overall

MEDITECH continues to manage the largest base of legacy EHR customers among vendors, with over 400 hospitals still using older platforms. A key success in 2024 was significantly improving its retention rate among these customers when they made decisions about their future EHR. Of legacy MEDITECH customers making a go-forward decision in 2024, 63% chose to migrate to the MEDITECH Expanse platform, more than double the 30% retention rate seen in 2023. Customers, especially smaller hospitals, cited the enhanced technology available via MEDITECH as a Service (MaaS), potential value, and stable vendor relationships with good executive involvement as reasons for staying.

Despite this improved retention, MEDITECH experienced a net loss of 57 hospitals overall. This was largely driven by one large health system moving 41 hospitals from Expanse to Epic. Of the 23 organizations that competitively replaced MEDITECH, 19 chose Epic (13 core Epic, 6 Community Connect), often citing interoperability benefits with nearby Epic organizations. MEDITECH did gain 11 specialty hospitals, primarily through existing health system customers standardizing on MEDITECH. MEDITECH holds an estimated 14.8% of the hospital market share and 12.7% of the bed market share.

Performance of Other Acute Care EHR Vendors

- Altera Digital Health: Saw no net-new contracts or migrations in 2024. Existing customers using the Paragon platform are focused on upgrading to its web-enabled version, Denali. Efforts to enhance partnerships and technology have improved customer satisfaction and optimism, though future stability remains to be seen. Paragon demonstrated better customer retention than the Sunrise platform within the Altera portfolio in 2024. The vendor saw a net loss of 19 hospitals.

- TruBridge: Migrated 2 hospitals from legacy systems. It remains a viable option for small hospitals with budget constraints. Efforts to improve partnership and product led to slightly higher customer satisfaction and a net increase in bed market share, though the vendor still had a net loss of 8 hospitals. Most losses were to MEDITECH or Epic Community Connect.

- MEDHOST: Secured no net-new contracts in 2024. Following its acquisition by Harris Healthcare (announced Jan 2024), customers noted some updates but reported uncertainty about the long-term plans for the system. MEDHOST saw a net loss of 4 hospitals.

- Azalea Health: Received very little market consideration in 2024 and lost 1 hospital, resulting in a net loss of 1.

Market Share Landscape and Methodology

As of the end of 2024, the estimated US acute care market share by percentage of hospitals stood at: Epic (42.3%), Oracle Health (22.9%), MEDITECH (14.8%), TruBridge (7.6%), Altera Digital Health (3.0%), MEDHOST (2.3%), Azalea Health (0.4%), and Other (6.7%). Market share by percentage of beds was: Epic (54.9%), Oracle Health (22.1%), MEDITECH (12.7%), Altera Digital Health (3.0%), TruBridge (2.4%), MEDHOST (1.2%), Azalea Health (0.1%), and Other (3.8%). KLAS determines market share based on validated, executed contracts for core acute care EHR replacements or new implementations occurring between January 1 and December 31, 2024. A “win” is credited to the newly contracted vendor, and a “loss” to the vendor being replaced. Migrations from a legacy platform to a go-forward platform from the same vendor do not count as net wins or losses for multispecialty hospitals but are tracked separately. KLAS relies on public information, vendor-reported data (validated with providers), and thousands of conversations with healthcare organizations. The firm acknowledges limitations, including lack of participation from some vendors (notably Oracle Health in 2024) and potential variations in the data.