_(52748025943).png)

_(cropped)-(1).jpg)

SBTi proposes more flexibility in 132-page net-zero overhaul

Window is now open for corporations, NGOs, regulators and others to offer feedback on “initial consultation” draft Corporate Net Zero 2.0. The post SBTi proposes more flexibility in 132-page net-zero overhaul appeared first on Trellis.

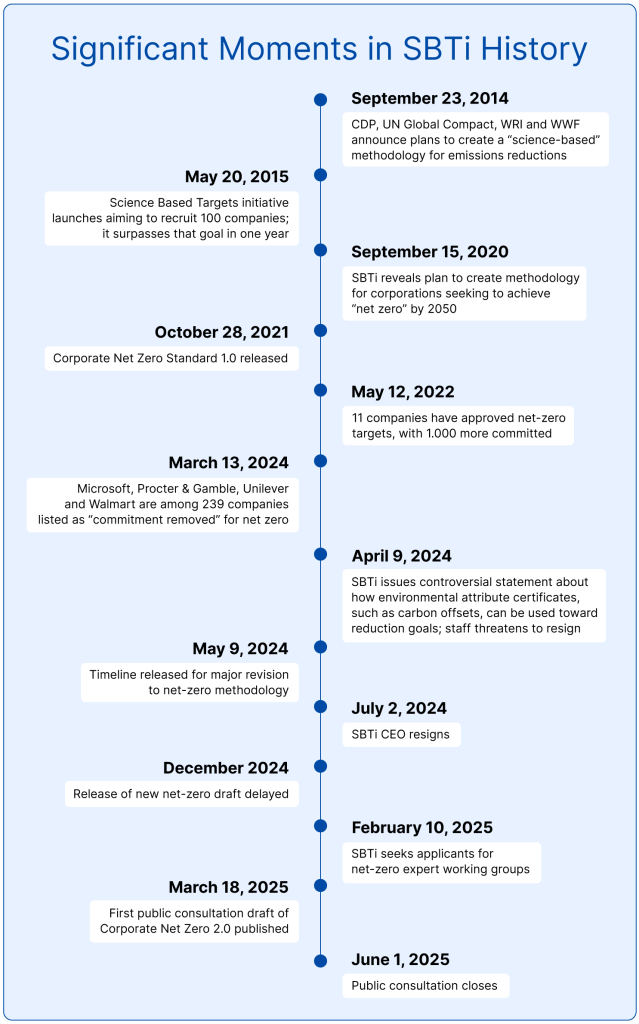

The Science Based Targets initiative has published a 132-page “initial consultation” document describing proposed revisions to the Corporate Net Zero Standard.

SBTi’s methodology has become the de facto framework that guides companies in setting science-based targets for emissions reductions that seek to hold global temperature increases below 1.5 degrees Celsius by 2050.

The draft has been delayed for months amid arguments over SBTi’s direction and a CEO resignation. More than 3,000 companies have announced plans to commit to net zero. About half have actually had their targets validated, and about one-third are small or midsize companies.

Nothing in the proposal published March 18 is technically final. SBTi has assembled five expert working groups to critique the revisions. It is also soliciting feedback via an online survey until June 1. From there, revisions will be made, and a new draft will be circulated for another round of comments before SBTi’s technical team and board consider them for approval.

Sweeping changes to Scope 3 methodologies

Some changes proposed in the draft will be tougher for companies to meet than the current net-zero standard, but SBTi is more flexible about requirements some corporations have criticized — especially its methodology for Scope 3 emissions from corporate supply chains.

More than half the companies surveyed by SBTi pointed to handling Scope 3 as their most significant challenge when aiming to become net zero. Revisions proposed in the draft would dramatically change that process. Key examples:

- Scope 3 targets are mandatory for big companies (those with more than $450 million in revenue), regardless of the percentage they contribute to overall emissions.

- Companies will need to identify their most emissions-intensive activities — sources that account for at least 1 percent of Scope 3 or that generate more than 10,000 metric tons of carbon dioxide equipment per year.

- SBTi proposes dropping the fixed percentages it previously applied for setting Scope 3 targets in favor of a system that would allow companies to focus instead on “relevant” categories — those that account for at least 5 percent of their Scope 3 footprint.

- Companies must use “direct influence” to require tier one suppliers (those with which it has a direct relationship) to set their own net-zero targets.

- Targets can take different forms — ranging from absolute emissions reductions to proof of “net-zero-aligned” procurement activities, such as buying steel or cement from suppliers that are reducing their production emissions in line with a plan to reach net zero.

- SBTi is more open to the idea of “indirect mitigation” of activities that companies can’t directly control. That might mean, for example, buying sustainable aviation fuel certificates through a book-and-claim system to reduce emissions related to air travel. It could also mean setting other procurement targets for lower carbon versions of materials that typically have high emissions, such as steel or concrete.

Under consideration: Recommendations for carbon removal targets

The path to net zero has always recognized the need to let companies abate residual emissions at the end of their journey; usually less than 10 percent of the carbon footprint for their baseline year.

The draft includes suggestions that would let companies get credit for “high-integrity” carbon removal activities taking place between now and their net-zero target year (usually 2050).

Here are three pathways being considered as part of the new consultation:

- Option 1: Require companies to set carbon removal and abatement targets for the near term and long term aimed at mitigating projected residual emissions in their net-zero year.

- Option 2: Recognize companies that set near-term and long-term carbon removal and abatement targets for that purpose.

- Option 3: Give companies flexibility for how they address residual emissions.

The options above pertain specifically to residual emissions that a company isn’t able to abate by its net-zero year. SBTi is also exploring whether to “recognize” companies for using carbon credits and other mechanisms to address the annual emissions generated as companies transition to net zero, which it refers to as “ongoing” emissions. But the draft doesn’t go into detail about what form the recognition would take.

Stricter governance expectations and other notable changes

The update proposes different criteria for large and small companies; there are also nuances related to geography. And all this is just the tip of the iceberg. Companies will also need to:

- Set net-zero goals more quickly. Once large companies commit to setting targets, they’ll have one year to deliver instead of the two years they previously had to get validated. Smaller companies still get two years.

- Anticipate spot checks. The draft suggests “any company and target” is subject to random assessments to confirm conformity with the standard and ensure integrity. Potential triggers for that sort of scrutiny include a credible complaint.

- Brace for regular baseline data evaluations. SBTi wants companies to reevaluate their base year emissions on an annual basis and whenever there’s a big organization change, such as a merger or divestment.

- Write a climate transition plan. The draft recommends publishing one within 12 months of having a net-zero target validated. These are disclosures that describe investments and business model changes a corporation must make to hold global temperature increases to 1.5 degrees Celsius. Roughly one in four companies that make voluntary annual disclosures to researcher CDP do this.

- Keep close scrutiny on baseline years. The organization wants them to be “representative of actual structure and performance.” Previously, it allowed companies to reach as far back as 2015. The revision would require companies to pitch a baseline no earlier than three years before their initial validation. Plus, big companies will need a third party to assure their emissions inventory calculations.

- Shift to better data collection processes. SBTi is pushing for companies to demonstrate more use of primary data, and for continuous improvements in how they trace emissions from suppliers. Full traceability for their most emissions-intensive activities is expected by 2035.

- Renewals could be required more quickly. Targets are typically set in five-year cycles. After that period, companies need to set new ones. Certain events could force an earlier renewal, such as the divestment of a business line or the need for a baseline year emissions recalculation.

Window for public consultation open

The organization will consider input on all of the revisions in the Corporate Net Zero 2.0 draft between March 18 and June 1.

Over the summer, SBTi will review the feedback to determine where adjustments or clarifications are needed; it plans to publish a summary of that input and how it is being addressed, but no specific timeline for that process has been disclosed.

Changes will be incorporated into a new draft that will be circulated for a second public consultation, before it is ultimately submitted for approval by the SBTi technical council. The final step for adoption is a vote by the SBTi board of trustees.

“This is an iterative process and the public consultation will help us identify the changes we can make to ensure SBTi’s revised standard creates impact at scale as effectively as possible,” said Alberto Parillo Pineda, chief technology officer at SBTi.

For 2025 and 2026, companies can still set science-based emissions reduction targets for 2030 using the existing Corporate Net Zero and Near-Term Criteria methodologies. Goals set in those years will be valid for either five years or until the end of 2030, whichever is earlier.

Starting in 2027, SBTi expects companies to set targets according to the finalized version of Corporate Net Zero Standard 2.0, due by the end of 2026.

Are you a corporate sustainability professional who’d like to discuss the proposed updates? Connect with me on LinkedIn (or email me) to start a dialogue.

The post SBTi proposes more flexibility in 132-page net-zero overhaul appeared first on Trellis.