.jpeg?#)

Don’t make us duplicate disclosures, companies tell California regulators

Businesses react to the country’s first climate disclosure laws. The post Don’t make us duplicate disclosures, companies tell California regulators appeared first on Trellis.

Key takeaways

- Ideas differ on what should define “doing business in California.”

- Many companies would prefer to avoid the new requirements altogether.

- Emissions and climate risk disclosure will help spur companies to better manage risk.

In more than 240 comments on California’s new climate disclosure laws and their implementation, companies, investors, trade groups and others urged regulators to base their requirements on already widely used reporting standards.

A review by Trellis of about 100 of the comments, submitted in response to a request from the California Air Resources Board, showed that businesses overwhelmingly prefer that the rules follow Task Force on Climate-related Financial Disclosure (TCFD) recommendations. Many commenters specifically asked California to employ the International Sustainability Standards Board standards, which follow the Task Force guidelines and are required in the European Union’s new Corporate Sustainability Reporting Directive.

But on another major implementation question — what constitutes “doing business in California” — commenters’ were all over the map.

Bottom line: Most big companies are well on the way to preparing for climate risk and emissions disclosure requirements, since Europe and other jurisdictions are also soon to mandate them. But many companies would be just fine, thank you, if the California rules didn’t apply to them.

‘Avoid unnecessary burdens’

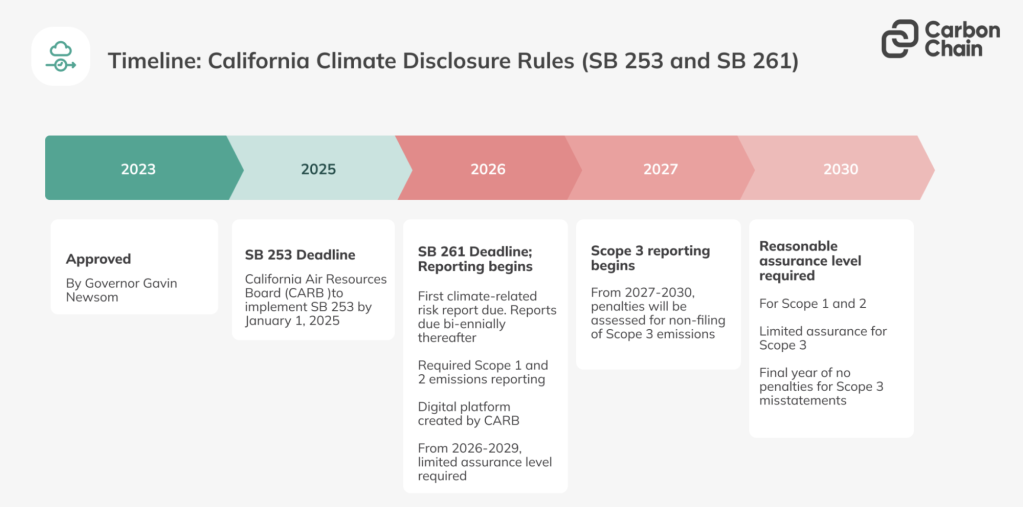

California’s Climate Corporate Data Accountability Act requires any company with annual revenues of more than $1 billion and doing business in California to annually report its Scope 1 and 2 greenhouse gas emissions starting in 2026 and Scope 3 emissions starting in 2027.

The Climate-related Financial Risk Act requires any company with more than $500 million in annual revenues and doing business in California to report climate-related financial risks and any measures it might be taking to reduce or adapt to them. Companies must start filing reports in 2026 and then every two years thereafter. Both laws require third party assurance.

The two laws were passed in 2023 and slightly amended last year. Even as the federal government abandons the idea of climate disclosure requirements, laws in California — the world’s fifth-largest economy — will affect many businesses in the U.S. and overseas.

“This ground-breaking legislation is set to reshape corporate reporting standards, with ripple effects outside California,” said the Mayer Brown law firm in guidance to companies. Since the U.S. Securities and Exchange Commission in March dropped its plans to mandate climate risk disclosures, California is the only U.S. jurisdiction requiring them, though several other states are considering similar legislation.

The California Air Resources Board asked specifically if it should mandate a strict set of standards based on the Greenhouse Gas Protocol and TCFD guidelines, and what should constitute “doing business in California.” It received an earful.

“We encourage all standard setters, wherever they are located, to set globally harmonized and aligned reporting legislation that avoids unnecessary burdens for businesses — interoperability with each other is a prerequisite,” wrote IKEA USA Public Affairs Leader Doug Murray. “A parent company reporting to EU CSRD standards should not have to disclose the same information in a different format and/or in another jurisdiction on behalf of one of their subsidiaries.”

California-based eBay, which operates everywhere, concurred. “The most important goal of CARB’s implementation should be to ensure interoperability with other reporting standards,” wrote eBay Chief Sustainability Officer Renée Morin. “eBay is already reporting climate risks and greenhouse gas (GHG) emissions voluntarily and is subject to mandatory climate reporting requirements in jurisdictions such as the European Union.”

Credit: CarbonChain

Asset managers applaud

Numerous asset managers — including Generation Investment Management, Impax Asset Management, Boston Walden Trust, Parnassus and Trillium Investment Management — recommended adoption of the Financial Reporting Standards Foundation’s International Sustainability Standards Board Standards, which also are the basis of the European rules. The asset managers also applauded California for requiring disclosure, since investors strive to assess climate-related financial risk when making decisions.

“As investors we seek consistent, reliable and comparable global reporting of climate-related risks and opportunities in order to make sound investment judgments,” wrote Generation Investment Management.

‘Unwarranted and costly’

The California laws do not define “doing business in California” despite using those words. CARB asked if the definition should be the same as the one in the California Revenue and Tax Code. But experts maintain that the state code’s definition is too wide, since it could cover companies with as few as one employee in the state or minuscule sales.

“The current approach to business identification represents an unwarranted and costly expansion of regulatory oversight that fails to consider the existing compliance burdens on businesses,” said the Manufacturers Council of the Central Valley.

The Western States Petroleum Association opposes using the tax code definition, saying “the provision’s thresholds are incredibly low.” Instead it says CARB should adopt a definition “based on the entity’s GHG emissions levels from direct emissions in California.”

“There’s a lot of pressure to establish a de minimis definition,” noted Jake Rascoff, director of climate financial regulation at the Ceres Accelerator for Sustainable Capital Markets.

Mind the gaps

For CSOs at companies affected by the California laws — or in states, like New York, likely to pass disclosure requirements soon — these responses indicate that the reporting rules are likely to mirror Europe’s CSRD, although what entities they apply to is an unsettled question. Nonetheless, companies should prepare, as they’ll need to measure Scope 1, 2 and 3 emissions and therefore institute measuring systems with suppliers and customers. The laws also require third party assurance of the reported data.

“These California climate laws add to the growing body of ESG reporting standards that are affecting U.S. companies — either directly by virtue of being in scope, or indirectly via a company’s value chain,” advised KPMG in a guide to the laws.

The U.S. Chamber of Commerce, which has fought numerous climate policies at federal and state levels, filed a lawsuit to stop the laws from taking effect, arguing California is trying to regulate emissions beyond its borders and violates the First Amendment by allegedly compelling speech. The U.S. District Court for Central California threw out part of the complaint but has yet to resolve the First Amendment claim.

Major consulting firms, meanwhile, are preparing their clients. PWC said that while many public companies already measure emissions and climate risk, thousands of private companies will also need to comply. PWC recommends they prepare by taking these steps:

- Assemble a cross-functional team.

- Determine scope.

- Understand the requirements.

- Create an inventory of existing climate commitments and related data.

- Assess the gaps between existing and required data.

- Develop a project plan for reporting climate data across their value chain.

The post Don’t make us duplicate disclosures, companies tell California regulators appeared first on Trellis.